quantlib.processes.heston_process.

HestonProcess¶

- class HestonProcess(HandleYieldTermStructure risk_free_rate_ts=HandleYieldTermStructure(), HandleYieldTermStructure dividend_ts=HandleYieldTermStructure(), Quote s0=SimpleQuote(), Real v0=0, Real kappa=0, Real theta=0, Real sigma=0, Real rho=0, Discretization d=PartialTruncation)¶

Bases:

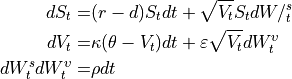

StochasticProcessHeston process: a diffusion process with mean-reverting stochastic variance.

- Attributes:

- kappa

- rho

- s0

- sigma

- theta

- v0

Methods

factors(self)size(self)